Recycling of tax-free cash

Recycling of tax‑free cash is where an individual boosts their pension savings by taking their tax‑free cash and increase their contributions into one or more pension plans to gain further tax relief. This process is closely governed by HMRC’s pension recycling rules, which exist to prevent individuals from exploiting tax advantages by reinvesting their tax‑free lump sums.

This article looks at when recycling may be considered an unauthorised payment and the conditions that determine whether a recycling event has taken place.

Key facts

If recycling of tax-free cash takes place, the tax-free cash is treated as an unauthorised payment.

The conditions for recycling to apply are:

- payment of the tax-free cash

- amount of tax-free cash

- significant increase in contribution level

- contribution increase of more than 30% of the tax-free cash

- pre-planning

What is recycling of tax-free cash?

What is recycling of tax-free cash?

One of the benefits to an individual of recycling is that it allows further tax-free cash to be paid. The income taken from the pension plan is re-invested back into one or more pension plans and tax relief is applied. The individual will continue to benefit from tax efficient growth and will have access to a further tax-free cash sum at the point they take benefits from the plan.

Whilst income payments from pension plans are treated as taxable income, this can be effectively offset by the tax relief given when the payment is re-invested into the pension plan.

It is worth noting however that HMRC do not classify income from pension plans as relevant UK earnings, and therefore the individual will need to have relevant UK earnings from another source so they are eligible for tax relief on the re-invested payments.

Our article on Member pension contributions - tax relief and annual allowance explains all about tax relief on personal contributions.

This all sounds too good to be true

Unfortunately, to an extent it is. HMRC introduced recycling rules in 2006 as it was concerned that recycling could abuse the generous tax relief system. Anyone who falls foul of these rules could face unauthorised payment tax charges.

What are the pension recycling rules?

What are the pension recycling rules?

The recycling rule applies to all pension tax-free cash payments where contributions are significantly increased on or around the time the payment is made.

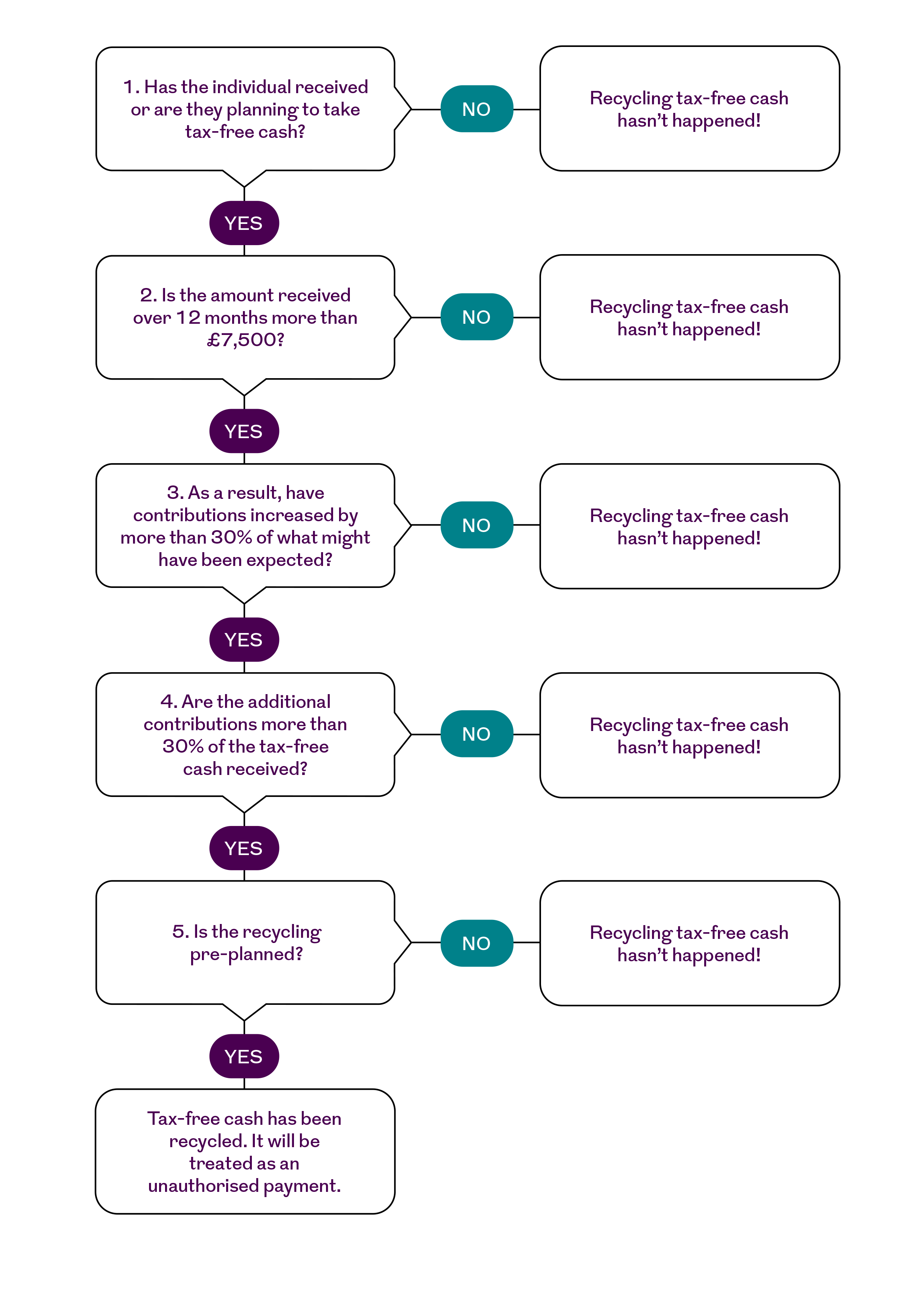

HMRC outline specific conditions to determine whether a recycling event has taken place.

Basically, if the answer is 'Yes' to all of the following conditions then bad things can happen. If the answer is 'no' to any of the questions below, then recycling of the tax-free cash hasn't happened.

What are the recycling conditions?

Let's take each of the above conditions in turn and look at them a little closer:

1. Payment of the tax-free cash

All payments of tax-free cash in a 12-month period need to be counted. This may include payments from more than one pension plan.

2. Amount of tax-free cash

Is the total of all tax-free cash payments over the 12-month period more than £7,500? If it's not, then recycling hasn't happened.

3. Significant increase in contribution level

Because of the payment of the tax-free cash, have the contributions increased by more than 30% of what might have been expected? This is obviously a lot easier to work out if there has been an established pattern of contributions. Where contributions haven't been paid in a while, HMRC allows RPI to be used to produce a current value for the contributions.

This applies to personal, employer and third-party contributions.

Contributions are measured over a five-year period to see if there has been a significant increase in contributions. This stops an individual getting around the rules by making gradual increases or increases just before the tax-free cash is taken. This five-year period is:

- the tax year in which the tax-free cash was taken

- the two tax years before the tax year that the tax-free cash was taken, and

- the two tax years after the tax year that the tax-free cash was taken.

So, if tax-free cash was taken in tax year 2024/25, the testing period would be from 2022/23 to 2026/27.

Any increase to contributions is measured on a cumulative basis over the five-year period – a running total of the additional contributions - when trying to determine whether a significant increase has occurred.

To look at what contributions would have been expected, the individual must look at the contributions in the years before the five-year period. So, if tax free cash is paid in 2026/27, then the five-year testing period for the 30% is tax years 2024/25 to 2028/29. It's then the contributions made before this so the pattern of contributions before 2024/25.

Recycling may not apply if their contributions increased because they are linked to salary, bonus, overtime, or commission as long as the basis on which the pension contribution is based hasn't changed.

4. Contribution increase of more than 30% of tax-free cash

The increase in additional contributions is only significant if the total amount is more than 30% of the tax-free cash. If contributions are paid to more than one pension scheme, it's the total of all contributions that need to be looked at.

As described in point 3 above, the increase is measured cumulatively over the 5-year period.

The fact that the individual had other money available that could have funded the greater contribution doesn’t mean that recycling is avoided. For example, taking a loan out or using savings to pay the contributions but paying the loan back or topping up the savings using the tax-free cash. This is because the individual always intended the tax-free cash to be an integral aspect of providing the contributions even if in an indirect way.

5. Pre-planning

If the answer to all the above conditions is 'yes', then it's going to all come down to the last condition. This is perhaps the hardest condition to interpret but let's have a stab at it.

In its simplest sense, pre-planning means that there was an intention right from the very beginning to use the tax-free cash as a way of significantly increasing pension contributions. To satisfy this condition, such pre-planning must take place at the 'relevant time'.

If a decision is made to use the tax-free lump sum to significantly increase contributions, this is pre-planning. The 'relevant time' is when the tax-free lump sum is taken. Even if the contributions increase before the tax-free lump sum is taken this can be pre-planning. In this case the 'relevant time' is when the contributions are increased.

HMRC Pensions Tax Manual - PTM133820: Recycling of tax-free cash - pre-planning

What are the consequences of recycling?

What are the consequences of recycling?

If an individual is caught by the recycling rules, the amount of the tax-free lump sum is regarded as an unauthorised payment and any of the following charges may be applied:

- an unauthorised member payment charge of 40% of the tax-free lump sum paid

- an unauthorised payments surcharge of 15% of the tax-free lump sum paid

- a scheme sanction charge of 40% of the tax-free lump sum

- a de-registration charge of 40% of the scheme's assets

However, not all of the charges are automatic.

HMRC Pensions Tax Manual - PTM133840: Deemed unauthorised payment and taxation

Case studies

Case studies

It's worth looking at a couple of case studies of where recycling does and doesn't apply:

Where recycling doesn't apply

Jim takes tax-free cash of £7,000 on 1 May with the intention of using it to pay significantly greater contributions to a registered pension scheme.

The amount of the tax-free cash doesn't exceed £7,500 and no other lump sums have been paid to Jim in the last 12 months. The recycling rule isn't triggered as the amount of the tax-free cash is less than £7,500.

Where recycling does apply

One month later, on 1 June, Jim takes more tax-free cash of £10,000 in order to further significantly increase contributions. The increased contributions amount to £10,000 and are more than 30% of the contributions paid before the five-year period.

As Jim has received another tax-free cash lump sum within the previous 12 months (the lump sum of £7,000 taken on 1 May), the £10,000 has to be added to the previous lump sum. The total amount exceeds £7,500 so the recycling rule is triggered. Here's why:

- Jim specifically took the tax-free cash of £10,000 in order to pay £10,000 back into a registered pension scheme as a tax relievable contribution.

- That lump sum of £10,000 (together with the earlier lump sum of £7,000) exceeds £7,500.

- The amount of the increase is more than 30% of what could be expected.

- The amount of the significantly increased contribution (£10,000) exceeds 30% of the tax-free cash of £10,000 (£10,000 x 30% = £3,000).

The recycling rule applies to the second lump sum, resulting in a deemed unauthorised payment of £10,000.

Where recycling doesn’t apply – example of cumulative basis

Linda takes tax free cash of £100k from her pension scheme in tax year 2024/25 and has made the following pattern of contributions:

Tax Year |

Contribution made |

|

| 2019/20 | £30,000 | |

| 2020/21 | £30,000 | |

| 2021/22 | £30,000 | |

| 2022/23 | £32,000 | Increase of £2,000 |

| 2023/24 | £32,000 | Increase of £2,000 |

| 2024/25 | £32,000 |

Tax-free cash taken this tax year of £100k Increase of £2,000 |

| 2025/26 | £38,000 | Increase of £8,000 |

| 2026/27 | £40,000 | Increase of £10,000 |

Cumulative increase of £24,000 (£2,000 + £2,000 + £2,000 + £8,000 + £10,000)

So, there is a history of regular contributions of £30,000 before the five-year testing period (tax years 2022/23 – 2026/27). During the five-year testing period, the cumulative increase of £24,000 is 80% more than what would be expected (£24,000/£30,000). The condition that the contributions increased by more than 30% of what might have been expected has been met.

However, the significant increase in the contributions (£24,000) doesn’t exceed 30% of the lump sum (£30k) so Linda doesn’t meet the requirements for recycling.

Disclaimer

The information provided is based on our current understanding of the relevant legislation and regulations and may be subject to alteration as a result of changes in legislation or practice. Also it may not reflect the options available under a specific product which may not be as wide as legislations and regulations allow.

All references to taxation are based on our understanding of current taxation law and practice and may be affected by future changes in legislation and the individual circumstances of the investor.